The Howey Test

Is Bitcoin a security? Howey should it be regulated?

This week President Biden signed an executive order called ‘On Ensuring Responsible Development of Digital Assets’, which signalled a positive regulatory stance towards crypto. In a nutshell, it says that the US wants to protect investors, but that they also want to be promote innovation and be a leader in the space. It calls for coordination amongst the different regulatory bodies to establish a clear and consistent framework for crypto regulation. Groovy.

Here is the timeline of what’s supposed to be happening and when.

{kind=link}

The problem is that there are 9 different financial regulatory bodies in the US, and who regulates what depends on which asset you’re talking about. And yes, you’ve guessed it - what the heck is a digital asset anyway and which of the 9 bodies should be regulating them?! This has the potential to turn into a monumental ‘my NFT is bigger than yours’ bun fight with plenty of postering and no progress. And on the sidelines there are a lot of crypto entrepreneurs wondering whether they’re going to end up in court for not being regulated properly.

But fear not - a man from an citrus grove will bring fruity order to the ensuing chaos. Meet Mr Howey.

The “Howey Test” as it has come to be known determines whether an asset is a security or not, and therefore whether the asset should be regulated by the SEC (the main US regulatory body called the Securities and Exchange Commission). Here’s the juice:

Mr Howey owned a citrus grove that was doing quite well, but he needed cash to expand. So he sold the citrus grove to an investor and leased it back off him through a service contract, under which Howey would use his skills to harvest the citrus grove and supply the investor with profits. Seems simple, but this got the US Supreme Court’s knickers in a twist as they deemed that the ‘investment contract’ that Howey had put in place with his investor was a ‘security’, and should therefore be regulated by the SEC. Big debate, massive fight, Howey lost, but the episode made everyone realise they needed a clearer definition of what should and should not be regulated by the SEC.

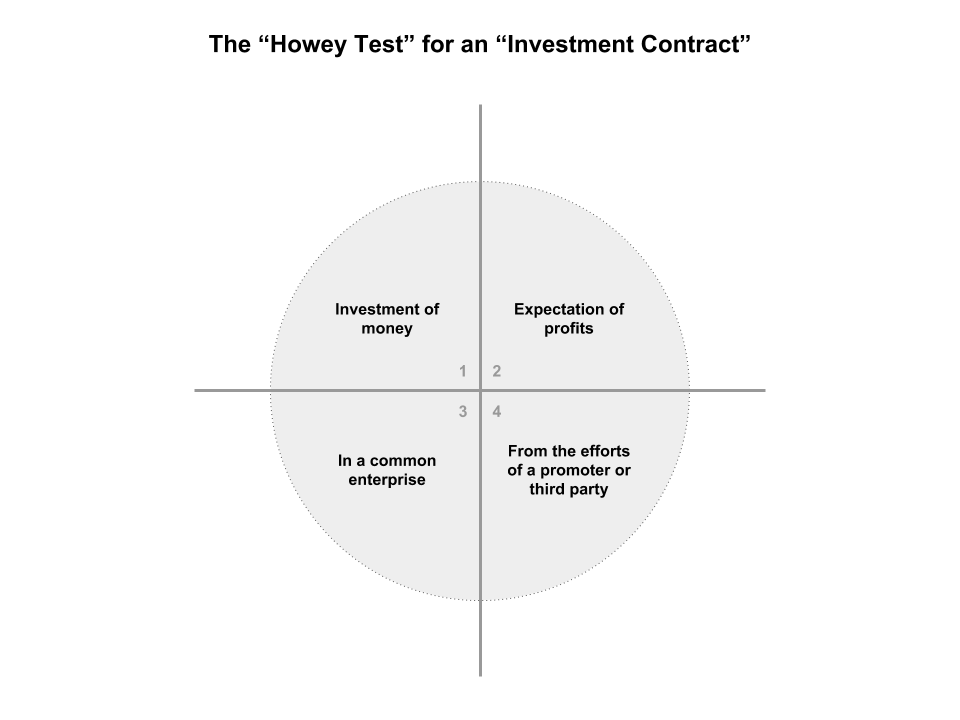

And so the Howey Test was born, and it determines that a security is an investment contract that has the following properties:

An investment of money

With the expectation of profits

In a so-called “common enterprise” (roughly meaning: investors and the company rise and fall together)

From the efforts of a promoter or third party (some dispute over whether this means “solely” from a promoter, but clear that it entails “significant managerial efforts” of a single promoter)

If the contract satisfies all 4 properties, it “passes” the Howey Test and is therefore a securities transaction. If the contract does not satisfy any one of them, it fails the Howey Test and is therefore is not a securities transaction - and therefore no need to worry about the SEC being on your back.

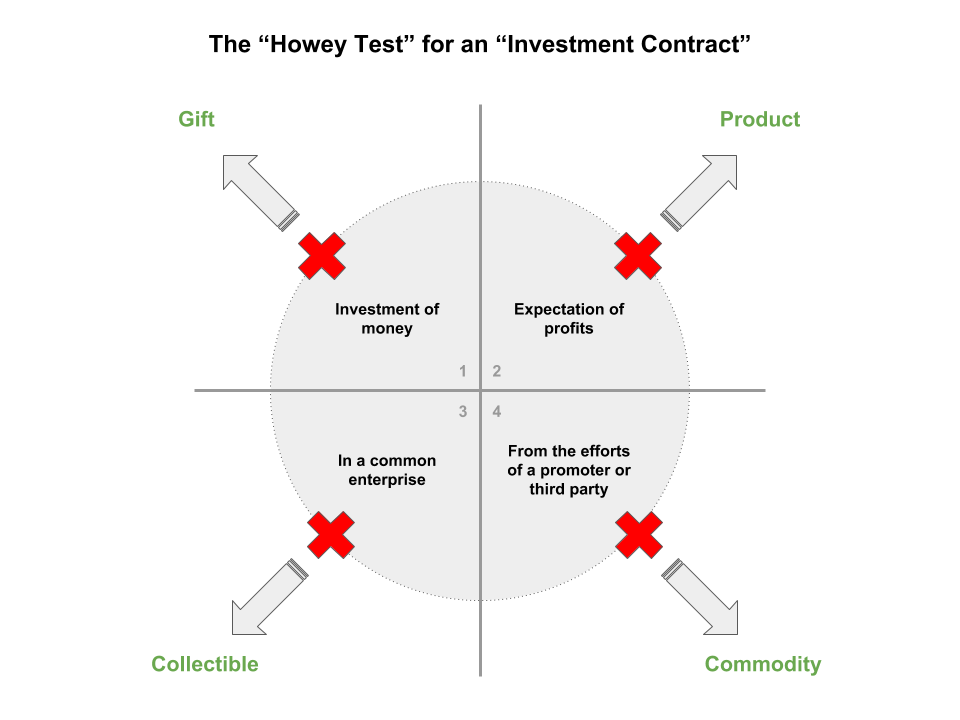

So with all of that as background, here’s how this works in context. All 4 segments need to be satisfied for the asset to be a security:

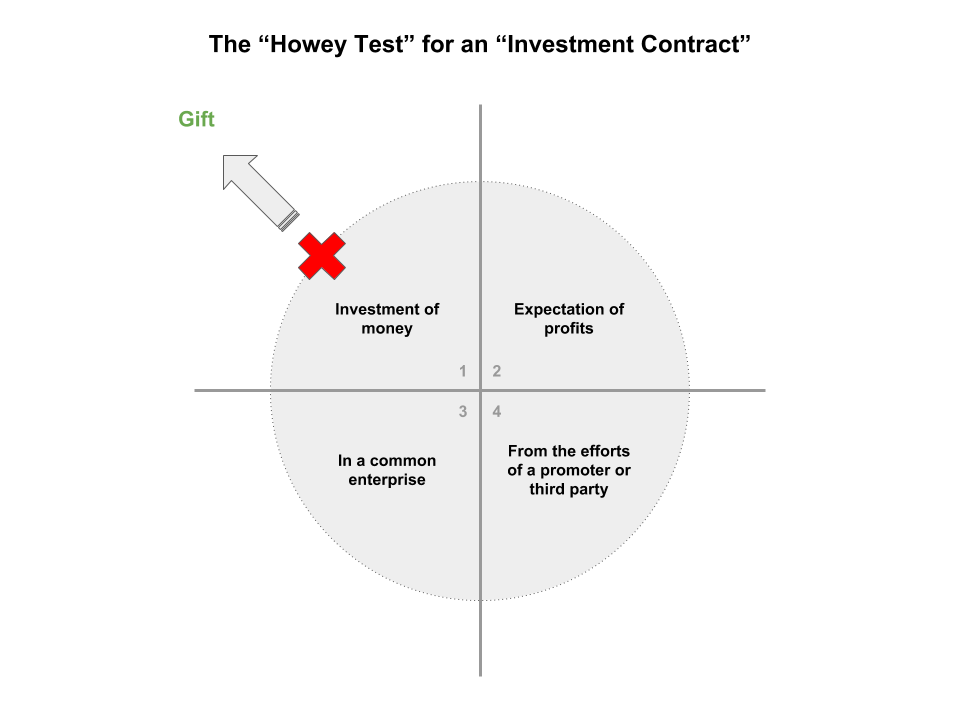

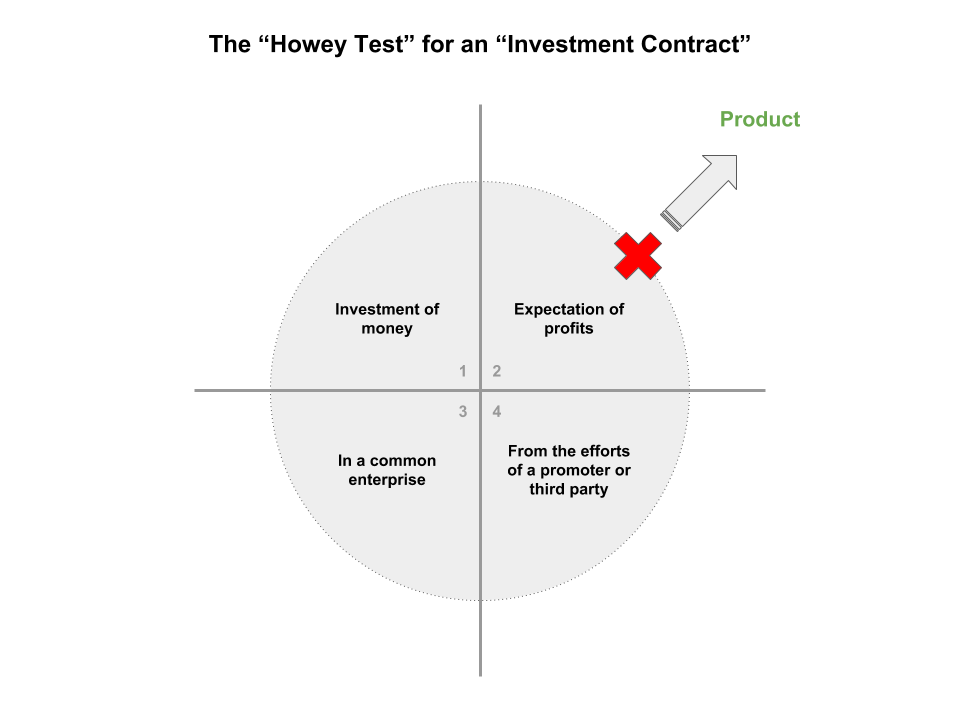

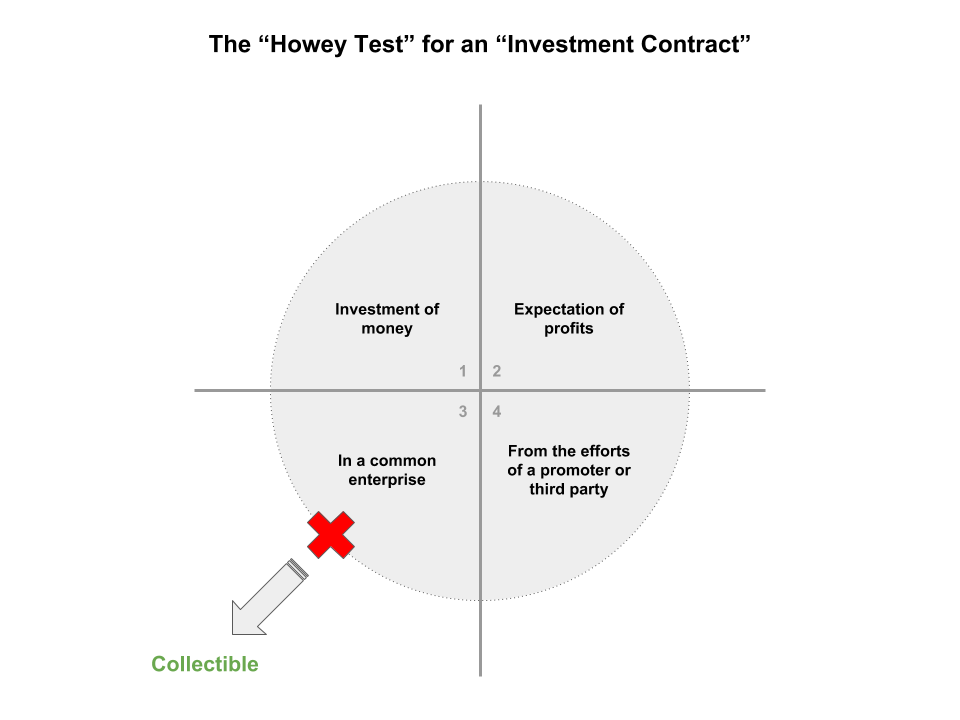

What happens if you remove each of the segments one-by-one?

1) Remove the “investment of money” and what you have looks more like a Gift (think: receiving airline miles, or ride credits on Uber, or “airdrops” of tokens in a crypto network)

2) Remove the “expectation of profit” and what you have looks more like a product (think: pre-buying a backpack or movie on Kickstarter, purchasing laundry or arcade tokens, or buying Stacks Tokens to insert records in the Blockstack blockchain):

3) Remove the “common enterprise” and what you get looks more like a collectible (think unique items like stamps, baseball cards, or CryptoKitties):

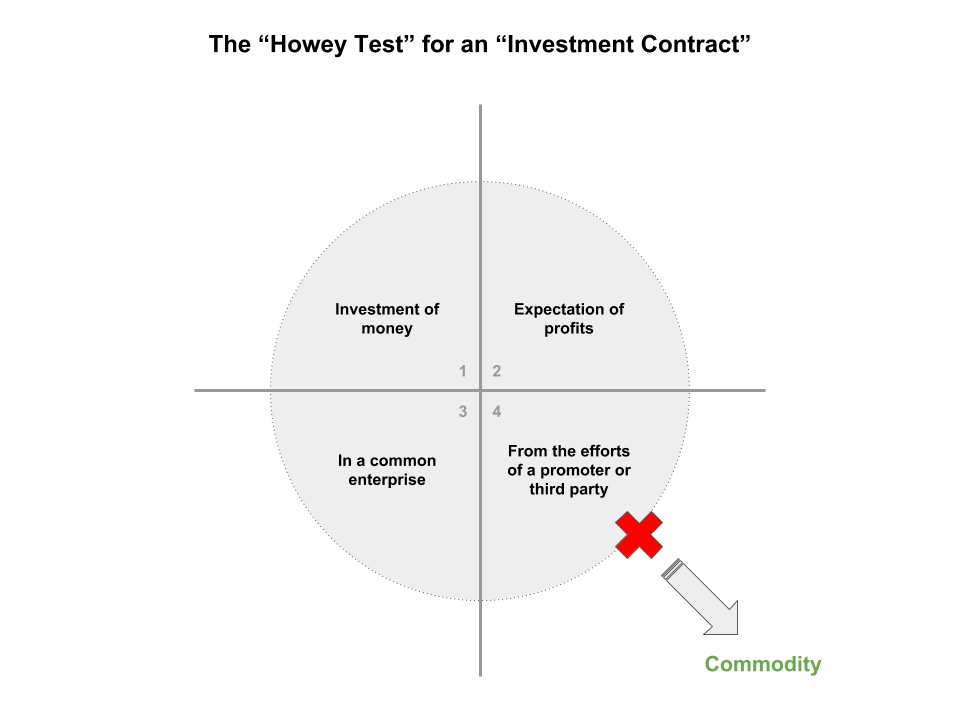

4) Finally, remove the “efforts of a promoter or third party” and what you get looks more like a commodity (think gold, wheat, or Bitcoin):

All together, it looks like this:

And so Bitcoin, which has never sought public funds to develop its technology, does not pass the Howey Test used by the SEC to classify securities, mainly because its profitability has never relied on the efforts of a promoter or third party.